Visual Overview

A chronological account of the proposed transaction to move Zashi from a public charity to a private company, from the Board's perspective.

Last updated: January 2, 2026

Disclaimer: This document reflects the recollections and perspectives of certain independent board members as of the date shown and is not a complete record of all events. It is provided for informational purposes only, does not constitute legal advice, and contains subjective characterizations that other parties may dispute. Nothing herein shall be construed as an admission of liability.

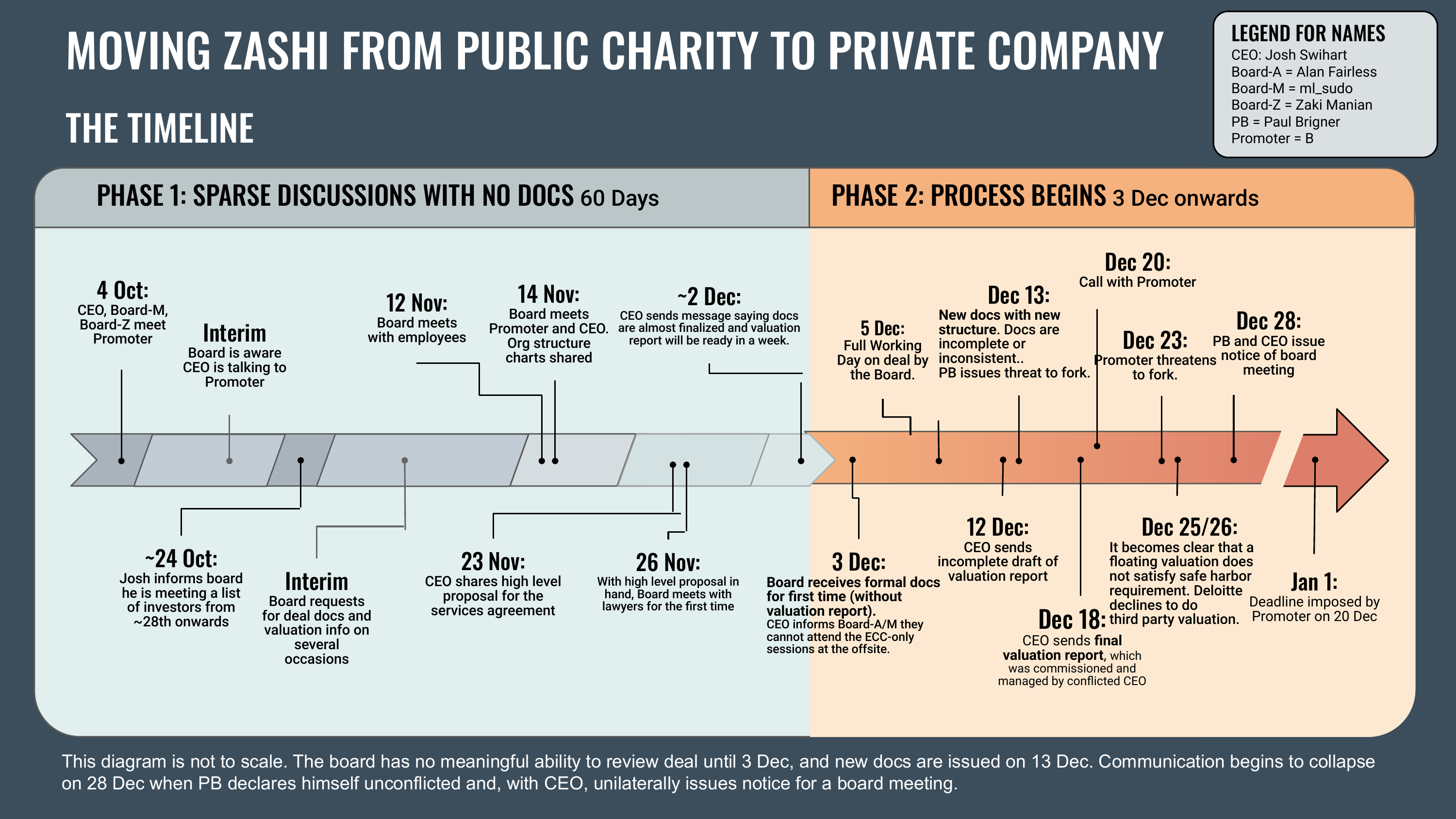

CEO, Board-M, Board-Z meet Promoter at a large group session after a crypto conference. No concrete plans were made, but both sides indicated interest in collaborating.

Board is aware CEO is speaking with Promoter. Board requests deal docs and valuation info on several occasions.

CEO informs the board he is meeting a list of investors from ~28th onwards. Independent directors hold an ad hoc meeting.

Board meets with a small handful of longtime employees.

Board meets with Promoter and CEO. Org structure charts are shared for the first time.

CEO shares a proposal for the services agreements between Bootstrap and NewCo. It emphasizes motivation for the deal and provides some high level structuring. It appoints PB as CEO of the remaining Bootstrap org.

With the basic proposal in hand, the Board meets with Bootstrap counsel for the first time. The board understands counsel previously raised issues with the CEO regarding the proposal. Lawyers provide extensive advice. The directors get up to speed on the standard, rigorous process that must be followed for related party nonprofit transactions.

CEO sends Board message saying docs are almost finalized with Promoter and Promoter's lawyers, and will send them to Bootstrap's lawyers before sending them to the board. The CEO says the valuation report will be ready in a week.

Board receives formal docs for first time; CEO requests for comments and signatures. Board-Z and CEO discuss on a call. Separately, CEO informs Board-A/M they can attend the ECC offsite but not the ECC-only sessions.

Full day working session for Board to analyze docs received, involving clearing full calendar schedules and changing travel itineraries.

Board-A/M/Z inform CEO of intention to attend all sessions of ECC offsite (which starts on 12 Jan). The CEO reacts strongly and construes it as an inappropriate assertion of power, adding that shareholders of the NewCo would not agree.

Board explains that under the contemplated proposal, the Board still has legal responsibility to ensure that charity funds are spent on mission-aligned work, so the Board needs to know what is being worked on. It is also not obvious that the deal will close fully before the offsite.

Board follows up with CEO with details of what needs to be done and valued to consummate the transaction, which have not yet been considered (including form of payment, transitional media access, etc). The board reminds the CEO that it needs to independently investigate any valuation even if there was a third party valuation.

The CEO protests and suggests adding "AI model valuation," and a letter from an investor group stating what they would pay.

Board chases for valuation report. The CEO sends a draft, but the draft only has final numbers and no qualitative explanation (i.e. difficult to interpret).

Board and Bootstrap lawyers unexpectedly receive new docs from CEO two hours before a call. The transfer of Zashi is prioritized and the services agreement is punted for later. Bootstrap lawyers provide legal advice, and the directors understand this as emphasizing the need to fulfill IRS safe harbor and that the board must satisfy very specific documentation requirements.

Proposed Resolutions don't fulfill the Safe Harbor standard.

The difficulty is not fixing the resolutions but that the process being run wasn't designed to fulfill the Safe Harbor. This left the board scrambling to fulfill a safe harbor compliant process.

Board resolution includes a statement that the board believes the deal has achieved the "Fair Price" requirement by reviewing three "independent" valuations:

Documents were inconsistent or incomplete:

On the call, Board attempts to explain the requirements of a legal deal, per the Bootstrap lawyer's memo, but CEO says it would be "superfluous… unnecessary." Board reminds conflicted director that the risks to him are the highest given his additional fiduciary duties; PB says he has "zero concern".

PB threatens Board to take the deal or else CEO would fork, take all the employees and Bootstrap would be left with nothing. Board says it has to run the process as prescribed by law. PB tells CEO he should fork now.

CEO invokes his power as ECC President to call a board meeting, adding the Promoter and INV. Board points out that he is a conflicted party and the independent directors should meet them without him.

CEO states his belief that any conflict is limited to deliberation and decision-making so his involvement should not be problematic. Conflicted director PB indicates interest in attending if possible.

CEO sends final valuation report. The report unexpectedly turns out to be a cost-based valuation and does not reflect comparables and revenues, which are basic inputs for a fair market valuation.

Board meets with Promoter and INV. Board indicates strong interest in Promoter being involved in the Zcash ecosystem, and emphasizes how hard it has been trying to sort out a deal with CEO.

Board proposes working directly with Promoter to speed things up, which is agreed to. Promoter suggests using floating valuation to defer the valuation process and get the deal signed first.

Promoter pressures Board to sign a deal by 1 Jan. Board-Z commits to working closely with Promoter over the holidays 24/7 to get a defensible deal done.

Board requests Coordinator (ECC employee) to arrange for a board-to-employee meeting on 29 Dec, as speaking to employees was important to Board before it signed. 5 Jan was also offered in case some could not attend on 29th.

Board-M/Z hold a call and correspondence with Deloitte and KPMG as potential valuation providers.

Call among Promoter, Board-Z and Bootstrap's lawyer.

Promoter opens the call by threatening to fork if deal is not signed.

Received asset transfer list with a list of assets that includes assets not covered in the valuation report.

Received SAFE from Promoter, with additional provisions to restrict Bootstrap's communications regarding ECC for 1 year (written permission required).

Received board resolution, again written for us by opposing counsel, to waive CEO and PB's conflicts of interest.

Informed Promoter that the current timeline is not possible.

Promoter suggests the Board appoint Board-Z to make all decisions on behalf of the board. The Board did not respond to this.

Board investigate the floating valuation concept with lawyers. Directors understanding based on this advice is that approving the deal with a floating valuation would mean that we can't comply with the Safe Harbor.

Deloitte declines due to infeasibility of timeline. Board decides to pause all valuation work.

Directors understanding of provided legal advice is that a waiver of CEO and PB's conflicts of interest would not work.

PB issues a notice for a board meeting to advance the deal, even though he is not on the Special Committee established to investigate the deal, claiming he has unconflicted himself by giving up employment in the NewCo. (Conflicted status a board determination, not a unilateral determination by a board member.)

Board learns that their instruction to schedule a call with employees on 29 Dec was not carried out. Board attempts to schedule a call directly with employees (but only has a few emails). The previously scheduled time would have been only 13 hours later, on Monday morning (US time), so Board instead schedules for a day later (30 Dec).

CEO foils the meeting by inviting all employees and Promoter to the board meeting called by PB (but he does not have proper authority to do this, as board meeting guests are invited by the board or its chair).

Deadline imposed by Promoter on 20 Dec passes.

From Oct 4 to Dec 3, the board had no formal documents to review despite repeated requests. The board had no meaningful ability to evaluate the deal.

Once docs arrived on Dec 3, new docs with a different structure were issued on Dec 13. At a Dec 20 meeting, the board was told to complete due diligence and close by Jan 1.

The valuation report was cost-based rather than market-based, and didn't cover all assets being transferred. The valuation process should not be managed by a conflicted party.

The proposed resolutions didn't fulfill IRS Safe Harbor requirements. The process wasn't designed to meet nonprofit transaction standards.

The board received multiple threats to fork the project if the deal wasn't signed on the promoter's timeline, despite clear legal problems.

A conflicted board member attempted to declare himself unconflicted unilaterally and called board meetings to advance a deal that would benefit him.

The conflicted CEO used his position as CEO of the seller org to conduct a process resulting in him being CEO of the buyer org, without meaningfully soliciting input from the default responsible persons of the seller org.